Sales Tax for Event Planners Is a Nightmare (And Nobody Warned You)

Part 5 of 10 in the Event Planner's Financial Survival Guide

Nobody gets into event planning because they love tax code. You got into it because you love creating experiences — the logistics, the creativity, the moment when a room comes together exactly the way you imagined it. And then someone asks you whether you're collecting sales tax on your services, and suddenly you're somewhere you did not expect to be. Sales tax for event planners is genuinely complicated. Not because the concept is hard, but because the rules are inconsistent, the stakes are real, and the guidance for event companies specifically is surprisingly thin. If you've been flying by instinct on this one, you're not alone — and it's worth taking a careful look.

The Rules Are Different in Every State

Let's start with the most disorienting truth about sales tax: there is no single answer. Whether event planning services are taxable, what components of an event are taxable, and at what rate — all of this varies by state, sometimes by county, and occasionally by city. In Texas, event planning services themselves are generally subject to sales tax. In California, services are generally not taxable, but the tangible goods you sell alongside them often are. In New York, the picture shifts depending on whether you're selling a bundled package or itemizing services and goods separately. In Florida, catering is taxable but other event services may not be. If you work across state lines — planning events in multiple states for corporate clients who operate nationally — you're potentially navigating a different rulebook for every engagement.

What's Taxable and What Isn't

Here's where it gets genuinely complicated for event planners: you often sell a mix of things. Some taxable, some not. Physical goods transferred to a client — centerpieces, branded merchandise, printed materials — are typically taxable in most states. Services — coordination, consulting, creative direction — are typically not taxable in many states. But when you bundle them together in a single contract, the rules get murky. In some states, if a bundled contract is "predominantly" a service, the whole thing is non-taxable. In others, you need to itemize and apply tax only to the tangible portions. Catering is its own universe. Prepared food is taxable in most states, but there are exceptions for catering on certain premises, food served in certain ways, events at certain types of venues. And if you're a planner who contracts catering on behalf of a client and bills them for it, your relationship to that catering charge — are you reselling it, or is it a pass-through? — affects how it's taxed.

The Resale Certificate Question

If you're purchasing items on behalf of clients with the intention of billing them as part of the event, you may be able to purchase those items without paying sales tax at the time of purchase — and instead collect and remit the tax when you bill your client. This is what a resale certificate is for. Using resale certificates correctly is one of the most important (and most misunderstood) financial practices in event planning. Using them incorrectly — claiming resale status for purchases that don't qualify, or not collecting the tax you were supposed to — creates real liability. Getting this right requires knowing, for each purchase, whether it qualifies for resale treatment under the rules of the state where the event is taking place. That's not a one-time decision. It's a decision you're making across every line item, for every event, in every state.

The Risk of Getting It Wrong

Sales tax compliance failures don't usually come knocking right away. They accumulate. An audit two or three years down the road can reach back through your records and assess tax on everything you should have collected and didn't, plus interest and penalties. For an event planning company doing significant annual revenue, that exposure can be substantial. And the worst part is that many planners who haven't been collecting tax correctly don't realize it — not because they were being careless, but because nobody ever clearly explained what applied to their specific situation.

Doing It Right

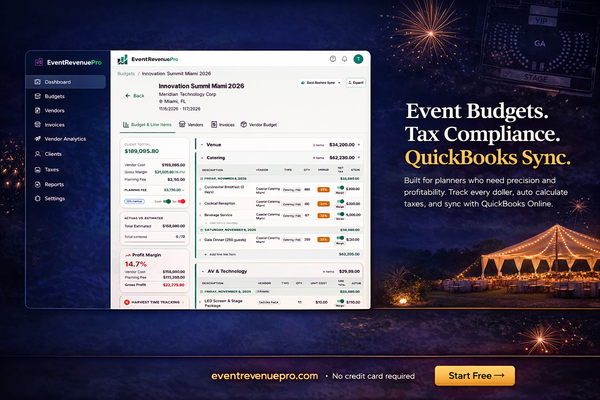

The foundation of sales tax compliance for event planners is knowing, for each event, what you're selling, where you're selling it, and which components are taxable under the rules of that jurisdiction. That means your budgeting and invoicing system needs to be able to distinguish taxable from non-taxable line items, apply the correct tax rate for the event location, and calculate the tax amount correctly — not as an afterthought, but as part of how the invoice is built. When tax is calculated as part of the invoicing process, with the right rate for the right jurisdiction applied to the right items, the risk of error drops dramatically. You're no longer making tax decisions in your head while building a spreadsheet at 11pm — the logic is built into the system. There are tools designed to handle exactly this complexity for event companies specifically, applying the right rules by state so you don't have to become a tax expert to stay compliant. It's one of those areas where having the right infrastructure genuinely protects you. In the next post, we're going to talk about what happens when a client disagrees with your invoice — and why your financial records are your best defense.

Next up: When a Client Disputes Your Invoice →

Event Revenue Pro was built to solve exactly this — a purpose-built financial platform for event planners, DMCs, and event agencies. Learn more →